The Magnificent Seven are more diverse businesses than their shared label suggests

The “Magnificent Seven.” It’s an understandable, memorable, and concise term, but its simplicity masks important distinctions. With the backdrop of strong U.S. stock market performance attributed to a handful of technology companies, the group’s run has fuelled questions about market concentration. When we look more closely, we see a clutch of U.S. stock market leaders that are more diversified than some may think.

The Magnificent Seven goes well beyond AI

Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla offer a wide range of products and services, with some areas of overlap. Certainly, their activities extend well beyond AI. The companies have a diverse footprint across industries, variously functioning as global marketplaces, cloud computing providers, and even automobile manufacturers and physical grocery store operators.

The Magnificent Seven business models span how we work, play, and consume

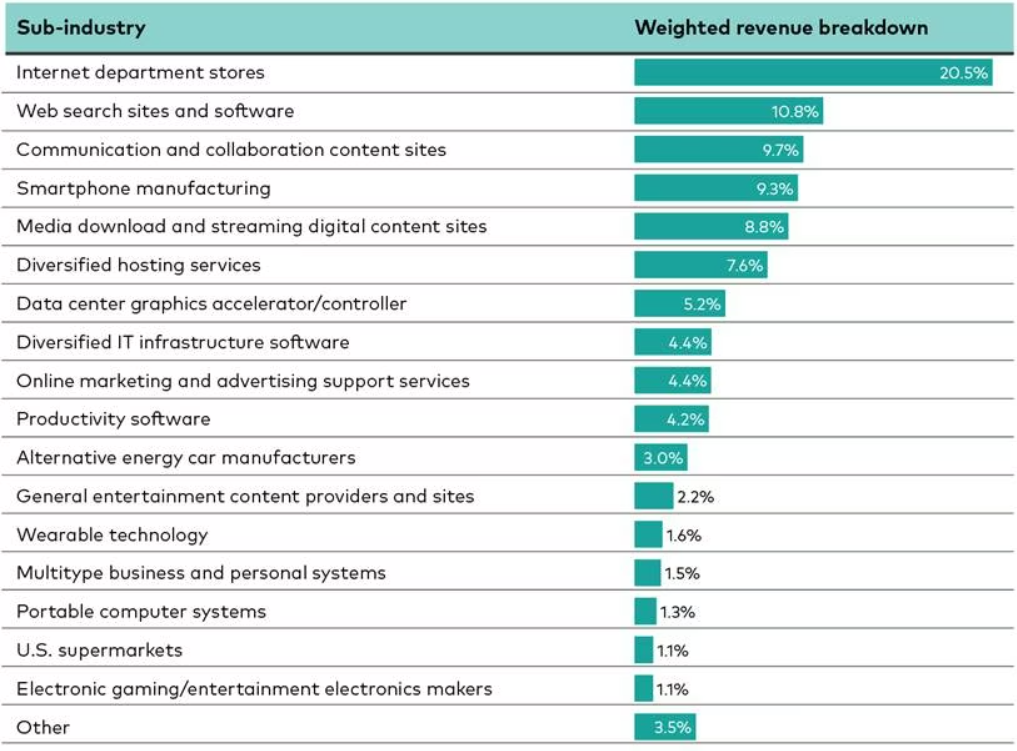

Sources of the companies’ combined 2025 revenues of $2.2 trillion

Notes: Weighted revenue breakdown is the proportion of combined revenues attributed to a given source. It is determined by aggregating the revenue from each source across companies and then dividing this figure by the total revenue from all companies combined. Revenues are based on the company’s reported annual fiscal year total revenue for 2025. Sum may not total 100% due to rounding.

Sources: Vanguard calculations, based on data from FactSet, as of January 2026.

Consider a few examples:

-

Amazon: Nearly two-thirds of its revenue comes from digital mall operations, approximately one-quarter from cloud services, and the remainder from online marketing and advertising services.

-

Apple: Half its revenue comes from smartphone sales, one-quarter from media downloads and content streaming, and one-quarter from a mix of computer hardware, cloud storage, and wearable consumer electronics.

-

Microsoft: Forty percent of its revenue comes from end-user home and office software, approximately one-third from back-end office infrastructure software, and the remainder from a mix of internet and data services, electronic gaming, and enterprise technology consulting.

While all three companies serve both consumers and commercial clients, their revenue exposures vary meaningfully across and within each company.

“The diverse revenue sources matter because they show that the Magnificent Seven’s business models span different end-users and markets,” said Erich Pingel, an analyst in Vanguard Investment Strategy Group. “Differences in business models also mean differences in risk-factor exposures, which helps explain why their stock prices do not move entirely in lockstep.”

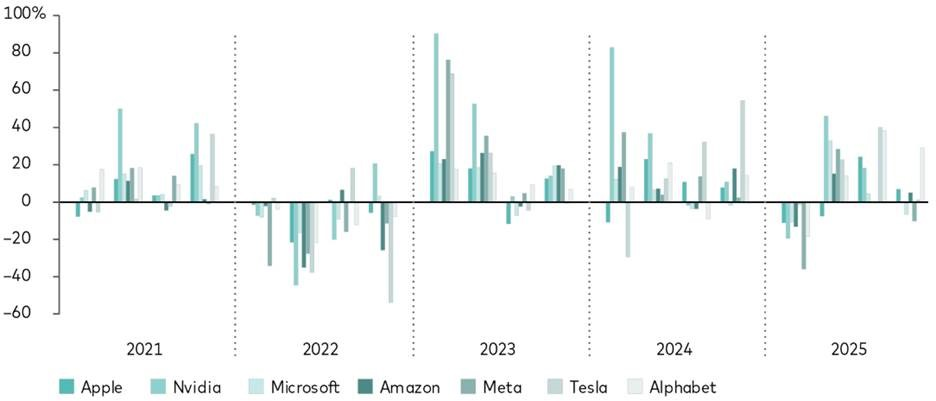

The Magnificent Seven stocks have not moved in lockstep

Quarterly total returns of common stocks, Q4 2020-Q4 2025

Sources: Vanguard calculations, based on data from FactSet, as of December 31, 2025.

Seven stocks: Neither narrow nor self-contained

“The Magnificent Seven currently represents around 30% of the U.S. stock market. The companies are often portrayed as a monolith, but their business models tell a different story,” said Rodney Comegys, chief investment officer, Vanguard Capital Management, and head of Global Equity. “Their commercial and equity market success coexists with meaningful differentiation at the company level—making it unlikely that all of them will disappear or experience significant drawdowns at the same time. They share a label, not a business model.”

For investors with long time horizons, it’s worth considering how creative destruction—the process by which innovation disrupts products, technologies, and companies—recasts market leadership.

Comegys said that those inclined to consider the market’s evolution over short periods should recognize that market leadership often changes—and that the human tendency to expect trends to persist is just one factor that makes it hard to predict who the new winners or laggards will be or when the transition happens.

The world is more interconnected and interdependent than ever, due in no small part to technological progress. Although the Magnificent Seven share common elements, the companies and their stocks are not interchangeable. Their business models, strategies, and consumer bases vary—and so has the performance of their stock prices.

Past performance information is given for illustrative purposes only and should not be relied upon as, and is not, an indication of future performance.

Actual results could differ materially from those referred to in the above statements. In particular, distributions and capital growth are not guaranteed. Investments in managed funds and exchange-traded funds are subject to investment and other known and unknown risks, including possible delays in repayment and loss of income and principal invested. Please see the risks section of each product’s PDS for further details. Neither Vanguard Investments Australia Ltd (ABN 72 072 881 086 AFSL 227263) nor its related entities, directors or officers give any guarantee as to the success of managed funds and exchange-traded funds, amount or timing of distributions, capital growth or taxation consequences of investing in such funds.

Source: Vanguard

This article has been reprinted with the permission of Vanguard Investments Australia Ltd. Copyright Smart Investing

GENERAL ADVICE WARNING

Vanguard Investments Australia Ltd (ABN 72 072 881 086 / AFS Licence 227263) (VIA) is the product issuer and operator of Vanguard Personal Investor. Vanguard Super Pty Ltd (ABN 73 643 614 386 / AFS Licence 526270) (the Trustee) is the trustee and product issuer of Vanguard Super (ABN 27 923 449 966).

The Trustee has contracted with VIA to provide some services for Vanguard Super. Any general advice is provided by VIA. The Trustee and VIA are both wholly owned subsidiaries of The Vanguard Group, Inc (collectively, “Vanguard”).

We have not taken your or your clients’ objectives, financial situation or needs into account when preparing our website content so it may not be applicable to the particular situation you are considering. You should consider your objectives, financial situation or needs, and the disclosure documents for the product before making any investment decision. Before you make any financial decision regarding the product, you should seek professional advice from a suitably qualified adviser. A copy of the Target Market Determinations (TMD) for Vanguard’s financial products can be obtained on our website free of charge, which includes a description of who the financial product is appropriate for. You should refer to the TMD of the product before making any investment decisions. You can access our Investor Directed Portfolio Service (IDPS) Guide, Product Disclosure Statements (PDS), Prospectus and TMD at vanguard.com.au and Vanguard Super SaveSmart and TMD at vanguard.com.au/super or by calling 1300 655 101. Past performance information is given for illustrative purposes only and should not be relied upon as, and is not, an indication of future performance. This website was prepared in good faith and we accept no liability for any errors or omissions.

Important Legal Notice – Offer not to persons outside Australia

The PDS, IDPS Guide or Prospectus does not constitute an offer or invitation in any jurisdiction other than in Australia. Applications from outside Australia will not be accepted. For the avoidance of doubt, these products are not intended to be sold to US Persons as defined under Regulation S of the US federal securities laws.

© 2026 Vanguard Investments Australia Ltd. All rights reserved.